Increased tech skills, the use of artificial intelligence (AI), and surviving the economy dominated the results of the 2024 Intuit QuickBooks Accountant Technology Survey of 700 U.S. accountants.

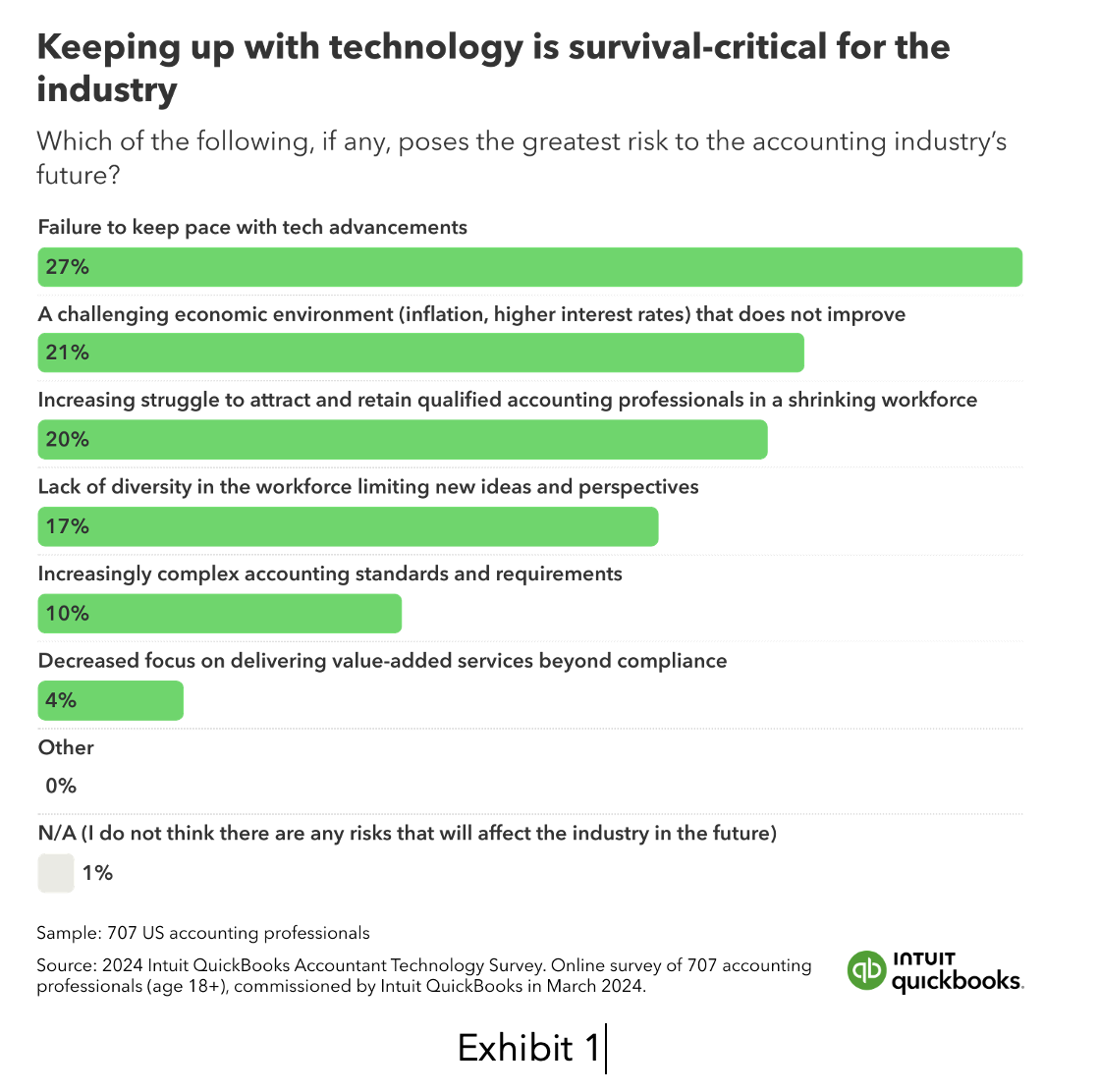

While the survey showed the profession has felt the shockwaves of changing economic conditions, failure to keep pace with technological advancements is the greatest risk to the industry, ahead of higher interest rates, the rising cost of goods, and widespread hiring challenges (Exhibit 1).

“The accounting profession has been experiencing a significant evolution at the intersection of technology and finance, presenting both challenges and opportunities for accountants to navigate as they strive to meet clients’ needs,” said Jeremy Sulzmann, vice president, Intuit QuickBooks Partners Segment. “QuickBooks is committed to helping accountants adapt to the industry’s changing landscape and adopt the necessary technologies to ensure their ability to innovate and succeed well into the future.”

Key Findings

In addition to the need to grasp technology, the survey revealed five other important findings:

- Nearly all respondents (98%) say they’ve used AI to help clients and their businesses over the last 12 months.

- Almost all (98%) have felt the headwinds of inflation and interest rates, but more than 9 out of 10 agree technology can help them—and their clients—to weather these challenges.

- More than 9 in 10 respondents who have outsourced work agree that outsourcing is another way to maintain business growth by improving efficiency and giving more time to focus on advisory services.

- Amid widespread hiring challenges, more than 9 in 10 agree the latest technology could help them solve skills shortages by helping to attract and retain talent.

- Client needs are increasing, particularly with financial and technology management, but technology is key to saving time and elevating advisory services.

Achieving Growth Through Technology and Education/Work Experience

To combat the threat of not keeping pace with tech advancements, many accountants are embracing and prioritizing the adoption of new innovations in their day-to-day operations. In short, investing in technology is important. On average, respondents reported they plan to invest $24,000 in accounting and bookkeeping technologies in the coming year, and 93% of respondents believe that accounting firms making more use of technology are more likely to survive periods of high inflation and interest rates.

“Integrating new technologies into your practice is extremely important as we move forward, especially with the pipeline issues we all face in our industry,” said Chris Picciurro, CPA/PFS, MBA, ARA, head of Integrated CPA Group in Franklin, TN, and Teaching Tax Flow, a proprietary system of personalized tax planning and strategy.

Picciurro suggest three ways to effectively integrate new technologies into your practice:

- Create a spreadsheet that details your technology stack and determines if there are overlap or gaps. Focus on processes, instead of people, running your business, and finding technology that can run the processes or automate them as much as possible. For example, using an online calendar app that integrates with your other apps and data collection is one amazing thing we use.

- Use something such as Intuit Mailchimp or another type of email communication tool, so that you can see what your clients are interested in, and communicate updates and important things with them all at once.

- I’m a huge fan of using videos and creating a video library for frequently asked questions, not only about taxes and accounting, but also about how you do business. This could include accessing your client portal or other frequently asked questions to save you time.

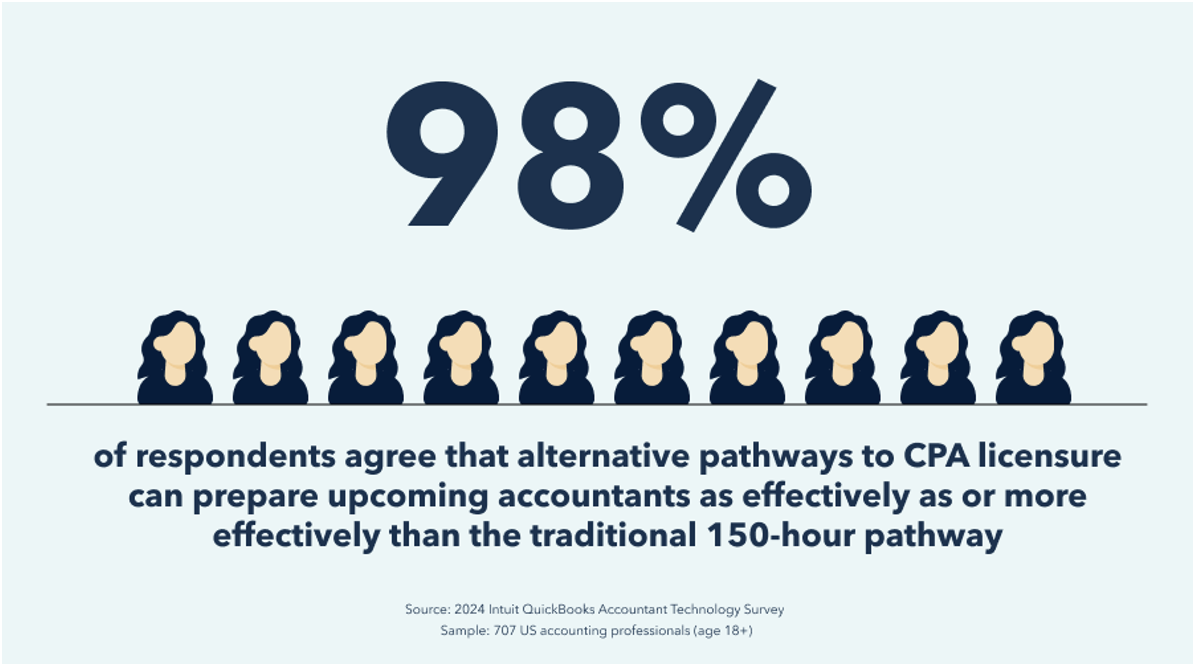

Technology adoption is also believed to have a positive impact on accounting skills shortages in attracting and retaining talent. Since 2023, hiring struggles persist, with 94% of respondents saying that hiring has been a challenge across the board—up 8 percentage points compared to last year’s QuickBooks data. This concern is growing as more respondents report experiencing hiring challenges for early-career professionals compared to last year, particularly for graduate and entry-level accounting roles. In fact, many accountants are calling for industry standards to shift in light of the talent pipeline shortage. Nearly all (98%) agree that alternative pathways to CPA licensure can prepare upcoming accountants as effectively as, or more effectively than, the traditional 150-hour pathway.

Blake Oliver, CPA, founder, and CEO of Earmark, and co-host of The Accounting Podcast, wrote an article for the Firm of the Future blog on rethinking the 150-hour requirement; he does not want to eliminate the requirement as much as offer a combined solution of education and on-the-job experience.

“The 150 hours of education and a year of work experience should remain an option, but we should return the 120-hour option with two years of work experience,” he said. “In essence, we’d allow future CPAs to swap the fifth year of education for an additional year of experience. Those who don’t want or need the extra education could start their careers and learn on the job.”

As for talent at any level, to attract and retain employees over the next year, nearly all respondents (99%) say their firms will prioritize the latest technologies to support day-to-day work. In addition, 95% agree that a willingness to learn and adopt new technologies is just as important to their success as traditional accounting skills.

The Impact of AI on Accounting

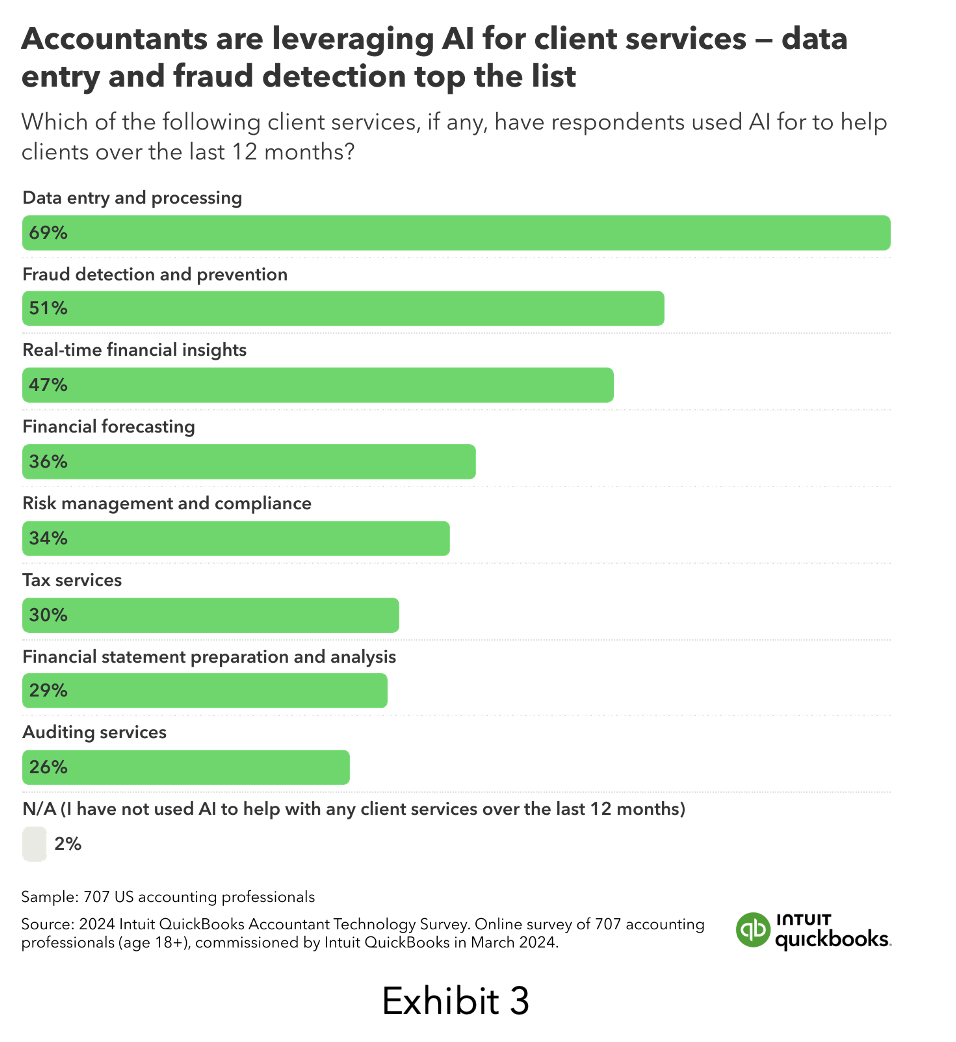

Staying ahead of the technology curve through the use of AI is growing in popularity to meet evolving demands. In fact, 98% of respondents have used AI to assist clients in the past year, and 98% have used AI for firm operations, with plans for expanded use.

Picciurro’s firm uses AI I for various tasks, including creating social media posts, editing important emails and documents, and conducting tax research.

“While it shouldn’t be relied on 100%, AI can be an invaluable tool for reducing the repetition of many tasks,” he said. “A good friend of mine, John Higgins, shared an important insight with me: AI won’t replace tax and accounting firms, but firms that use AI will replace those that don’t.”

Over the next 12 months, more than half of accountants say their businesses plan to invest in AI (57%) and automation tools (54%), highlighting the transformative potential of these technologies. This is a steady increase compared to last year, where a little under half (48%) of accountants said their businesses planned to invest in AI and automation tools.

While adoption of AI continues in the industry, many are approaching it with caution. For respondents, data privacy and security (31%), accuracy (21%), and implementation and maintenance costs (21%) ranked as their biggest AI concerns. Despite other reports noting that accountants are at high risk of being replaced by AI, only 9% in the industry felt that job replacement was a concern. To further ensure careful use of the tech, nearly all (99%) have formal ethics guidelines for AI use, and two-thirds (66%) say their guidelines include client disclosure for the use of AI in their work.

Navigating Economic Challenges

While adoption of new tech and innovation is the number one priority for accountants to successfully navigate through current economic conditions, our study also shows how accountants are assessing the threat from other economic forces.

According to the survey, one of the most significant challenges firms have faced so far in 2024 is reduced profitability, with 63% reporting a loss of profits due to higher interest rates and the rising costs of doing business.

“If you’re facing these kinds of challenges, my best advice would be to take a hard look at your client acquisition and pricing processes,” said Picciurro. “Too often, accountants undervalue their services and miss the mark on pricing. Developing a proper client acquisition process, coupled with a solid pricing strategy, is essential to remain profitable and scalable. I also encourage anyone struggling with this to find a group of peers or a mastermind group, and work together to share best practices.”

Just as accountants have faced financial challenges resulting from higher interest rates and rising costs, so have their clients. Nearly all respondents (99%) noted that higher costs and interest rates have adversely affected their clients. And 91% agree that while inflation has slowed, these economic factors still pose a threat to their clients’ growth over the next 12 months.

Read the complete 2024 Intuit QuickBooks Accountant Technology Survey results here. To learn more about how QuickBooks serves the accounting community with its integrated, end-to-end, AI-driven financial technology platform, visit FirmoftheFuture.

Survey Methodology

Intuit commissioned an online survey in March 2024 of 707 accounting professionals throughout the US, all aged 18+. More than 2 in 5 (44%) respondents own an accounting or bookkeeping business. More than 1 in 2 (56%) are employed by an accounting/bookkeeping firm as an accountant/bookkeeper. Two in 5 (41%) work for firms with more than 100 employees. Nearly 3 in 5 (59%) respondents work for firms with 0-99 employees. Percentages have been rounded to the nearest decimal place, so values shown in data report charts and graphics may not add up to 100%. Responses were collected using Pollfish audience pools and partner networks with double opt-ins, random device engagement sampling, and post-stratification based on census data to ensure accurate targeting and results. Respondents received remuneration.

Thanks for reading CPA Practice Advisor!

Subscribe Already registered? Log In

Need more information? Read the FAQs